With almost 4 in 10 Nigerians in debt, struggling to meet financial obligations has become a common concern. Nigeria’s economy has been marked by frequent currency devaluations and all-time high inflation rates, leading to relentless increases in the pricing of goods and services. As a result, 36% of households in Nigeria find themselves with some form of debt, ranging from loans from family to borrowing from banks and loan apps.

The pressure to meet regular financial commitments like rent, pre-existing loans, school fees, and health emergencies while trying to stay afloat can be overwhelming, leaving many trapped in a cycle of financial strain.

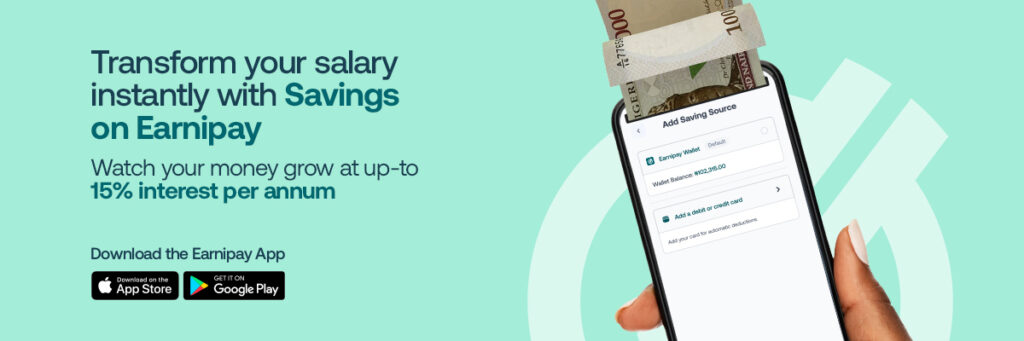

Setting specific savings goals and tracking your progress can be a powerful motivator, and it helps you stay focused and committed. Earnipay’s savings plan offers up to 15% interest per annum for at least 90 days, allowing you to progress toward achieving your goals.

“How much do I owe?”

Start by assessing your debts. How much do you owe? List all your balances, loans, and outstanding payments, noting the interest rates if any, minimum payments, and due dates. Doing this forms the foundation of your debt management strategy.

You’ll also have to map out your current income, expenses, and goals, This forms a roadmap, guiding your financial decisions and tracking your progress. Next, you’ll create a budget that aligns with lifestyle is crucial. ( Have you ever heard of the zero-based budget?). A budget helps mark funds for savings, spending, and debt repayment, ensuring you live within your means without feeling deprived.

“How Will I Pay It Back?”

Not all debts are created equal. Focus on repaying high-interest debts first, such as bank, car, or medical balances. Direct any extra funds towards your savings plan and try to keep minimum payments on others. This approach puts you on the path to becoming debt-free.

Here are some well-known methods to help you pay down your debt:

- Start by paying off your smallest debt first, then move on to the next smallest. This method focuses on the psychological benefit of seeing debts disappear, which can motivate you to tackle larger debts, even though it might not save the most money on interest. This is called the debt snowball.

- You can pay off your highest-interest debt first while making minimum payments on others. This method is best for those who prefer to save the most on interest charges.

- You can negotiate with creditors. Try to discuss options for modifying repayment terms, such as lower interest rates or extended payment periods. Many creditors offer hardship programs tailored to your situation, providing temporary relief while you work towards financial stability.

According to Dr. Alex Melkumian, founder of the Financial Psychology Center, becoming debt-free involves understanding what truly matters. Above all, maintain a positive mindset and stay persistent. Remember, no strategy is perfect—what’s important is to start small and keep moving forward.

If managing debt becomes overwhelming, seek help from financial professionals. Consult certified credit counselors or financial advisors who can provide personalized insights and strategies for navigating challenging economic circumstances. From debt to budgeting assistance, these experts offer invaluable support.

Leave a Comment